Eurex | Eurex Clearing | Eurex Repo

Fabienne Zamfiresco, Sven Jongebloed, Raul Schwab, and Gael Delaunay discuss how the evolving European market landscape will shape settlement and fragmentation in the region, and impact the Eurosystem

The European repo markets are vital mechanisms for sourcing collateral and securing funding, but the cost of participating in them has often been elevated by a fragmented and complex settlement infrastructure. This can raise capital costs for dealers, and has historically reduced netting opportunities that would alleviate impact on their balance sheets.

As such, repo can be one of the most expensive services that dealer desks offer. Recent reforms to market structure are set to change this however, as infrastructure providers facilitate settlement and collateral management. This could lead to significant balance sheet relief. Repo and reverse repo activity are reported on a gross basis, which has historically restricted liquidity providers’ ability to extend the service among their client bases. Netting is an obvious solution to freeing up balance sheet for expanded activity, but dealers must comply with certain IFRS and GAAP accounting standards to do so.

Achieving these requirements can be challenging when using the levers of current market infrastructure. The broad range of central securities depositories and cash accounts that market participants currently use to settle, represent a complicated system for trade processing in Europe.

However, significant changes to the ways market participants can settle repo trades are being introduced this year. These should bring down the balance sheet cost of participating in the market, allowing for an expansion in market activity and improve profitability.

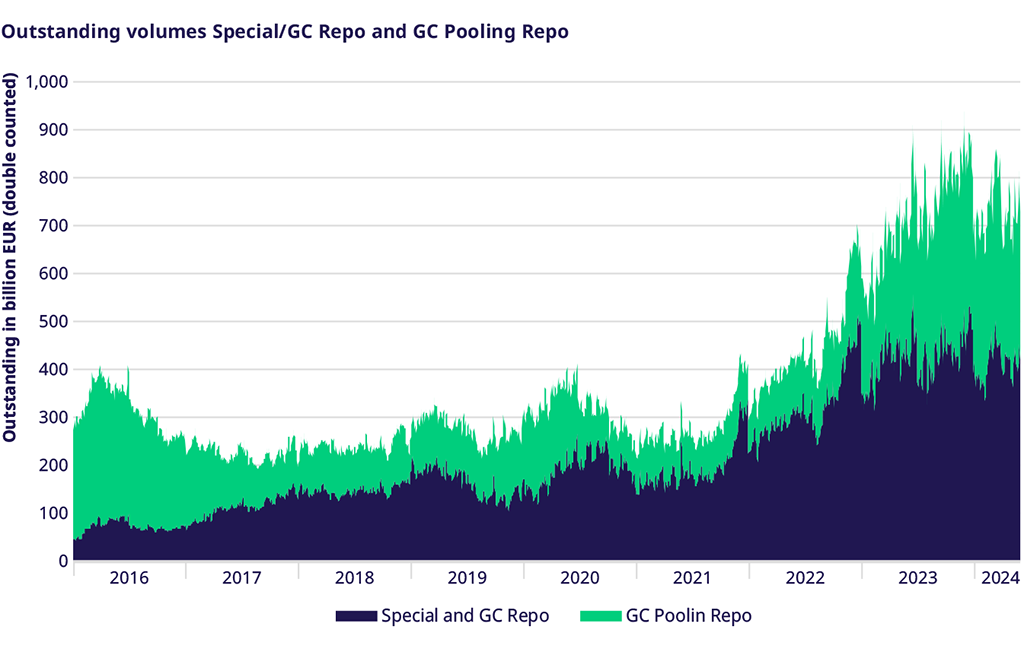

Building on previous integrations between Eurex’s GC Pooling and Special/GC repo segments, Eurex and Clearstream have enhanced their offering further, such that clients can now benefit from increased settlement efficiency, improved intraday liquidity management and reduced capital costs. Figure 1 shows the development of Special/GC repo and GC Pooling outstanding volumes whereby significant growth can be noticed since 2021.

To further examine the benefits these changes could bring, the following market specialists speak on the subject: Fabienne Zamfiresco, head of repo and securities lending desk at La Banque Postale; Sven Jongebloed, head of division, Securities Settlement and Collateral Management at Deutsche Bundesbank; Raul Schwab, senior associate vice president of product and business development at Eurex Repo; and Gael Delaunay, global head of collateral management at Clearstream.

What are the current pain points with settlement in the European market and what would be required to address these pain points?

![]()

Zamfiresco: The current pain points with settlement in the European market include fragmented market infrastructure, due to multiple different market infrastructures and legal frameworks across various jurisdictions. Risk of settlement fails is another challenge, as a shorter settlement cycle increases the risk of trade settlement fails, which can lead to penalties under the Central Securities Depositories Regulation’s (CSDR) Settlement Discipline Regime and additional costs for market participants. Addressing these pain points will require a coordinated industry effort, detailed impact assessments, and the development of a comprehensive implementation plan to ensure a successful migration to a shorter settlement cycle in Europe.

The ECB is going to introduce the European Collateral Management System this year. What are the expected benefits and will it reduce fragmentation?

![]()

Delaunay: The European Collateral Management System (ECMS) will replace the existing systems of the national central banks of the euro area that are currently used to manage collateral for Eurosystem credit operations. By implementing a single system, it ensures harmonisation across all national central banks. This streamlines processes and eliminates the need for interacting with different local collateral management systems. Furthermore, the ECMS will reduce duplication of effort and administrative overhead leading to operational efficiency and cost savings. By providing a consistent single collateral management system, the ECMS contributes to capital markets by facilitating the flow of cash, securities and collateral across Europe.

What changes are coming to EU settlement infrastructure and how will this enable greater balance sheet netting in the Special/GC repo and GC Pooling segments?

![]()

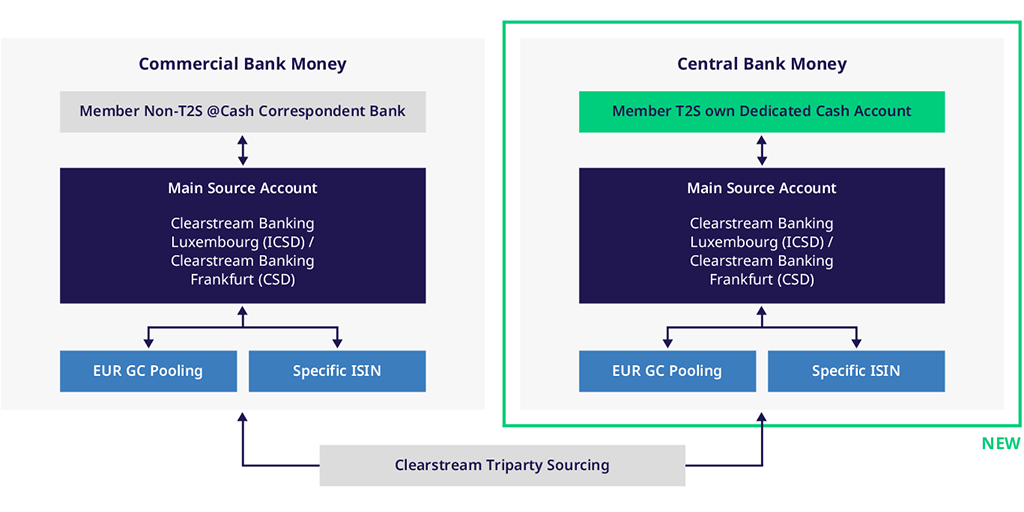

Schwab: For repo traders to achieve balance sheet netting in repo, they must meet five accounting conditions. These comprise facing the same counterparty, executing both repo trades on the same settlement date, having a master netting agreement in place and the availability of intraday credit facilities. There must also be an intent to settle on a net basis or simultaneously settle the two repo trades. We believe that settling Eurex cleared repos, including GC Pooling using a single CSD and cash account, ensures required criteria of achieving balance sheet netting.

From June, Eurex clients will be able to satisfy these conditions for the first time in central bank money by settling their GC Pooling and specific ISIN repo transactions at Clearstream Banking Frankfurt (CBF) in TARGET2-Securities (T2S), using a single dedicated cash account.

The extension to central bank money settlement for both specific ISIN repo and GC Pooling aligns with the introduction of the ECMS, which is currently planned for November 2024. Clearstream’s triparty connectivity to ECMS and extension of settlement of Eurex cleared repos to T2S at CBF, will allow for intraday liquidity management, improvement of operational efficiency and reduced capital costs and risk. Eurex and Clearstream believe that this will further support the attractiveness and stability of the European capital market.

How will greater recourse to central bank money benefit the Eurosystem?

![]()

Jongebloed: The Eurosystem supports the development and integration of pan-European financial market infrastructures. These infrastructures provide European financial markets with a single pool of euro liquidity in central bank money, ensuring safety, efficiency and integration. This is achieved through the use of TARGET Services and the pooling of financial transactions on payments, securities, and in future collateral. Additionally, the Eurosystem’s operational framework has evolved over the years. As excess liquidity gradually declines, the European Central Bank (ECB) Governing Council recently decided on changes to its framework in March 2024 to safeguard the smooth implementation of monetary policy for preserving price stability.