28 Aug 2024

Eurex | Eurex Clearing

The low touch future of FX derivatives

This is the third in a series of articles outlining the current views on FX futures. Subscribe to FX News to receive upcoming articles and updates!

The accelerating integration of over-the-counter (OTC) and listed FX derivatives markets is a story of change on multiple fronts. While regulatory shifts triggered the futurization of FX, technology will be the force that sustains its momentum.

Block trades and Exchange for Physicals (EFPs) are key to the growing interlinkage between OTC and listed FX markets. They create a bridge for sizeable trades sourced in the OTC FX markets to access the efficiencies offered by clearing in listed FX markets. As such, most major FX desks within banks are establishing low touch execution services for FX futures blocks and EFPs.

Changing norms

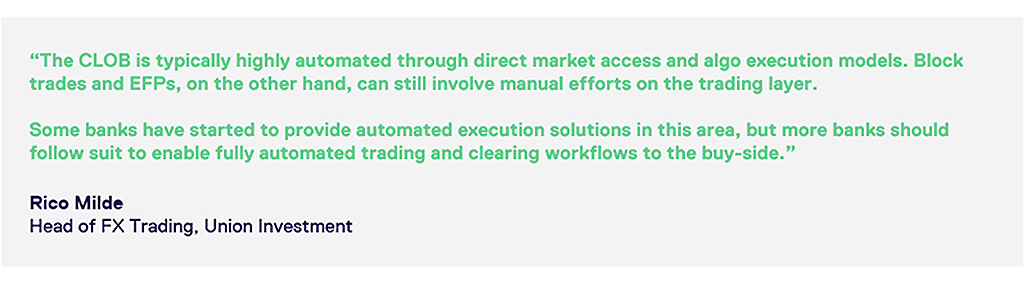

Execution in these corners of listed FX trading has traditionally relied on voice or chat message. This is a legacy of activity being managed by ETD desks – where trading outside the central limit orderbook (CLOB) was the exemption rather than the norm.

This is rapidly changing as demand for block trades and EFPs ratchets up. Banks are utilizing FX futures to reduce the capital costs that the SA-CCR regime – the standardized approach for counterparty credit risk – imposes on OTC instruments. Meanwhile, more buy-side firms are seeking solutions from the sell-side that keep them under UMR – uncleared margin rules – thresholds.

For banks, servicing client portfolios that are directional, uncollateralized and large has become much more expensive. As a whole, the business of providing FX swaps and forwards has become a lower margin one.

Banks therefore aim to transfer FX positions into the listed market. This can provide immediate cost savings to the bank and their clients – and clients can slip into well-established clearing pipelines.

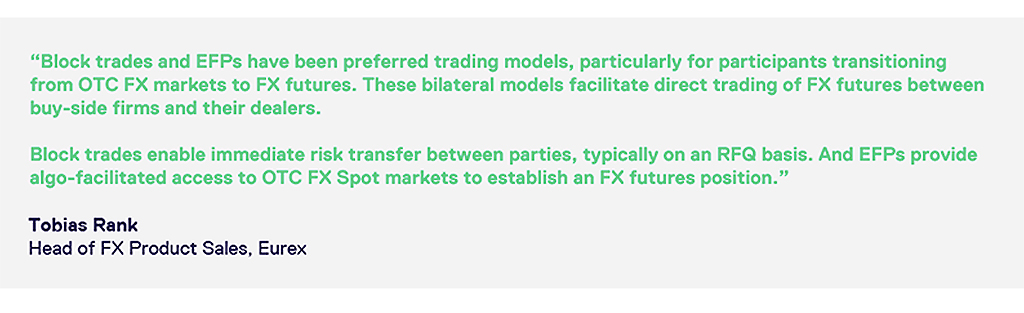

Through block trades, banks can offer OTC style liquidity in virtually any size to their FX futures clients. And with the help of EFPs, banks can offer OTC FX Spot access when building a client’s FX futures position. Both trading models are rapidly cementing their position in the FX derivatives market. As a result, most major FX dealers are expanding their FX futures offerings. And the growing relevance of FX futures has also peaked the interest of FX and e-FX desks - who are actively incorporating block trades and EFPs into their existing FX business.

Changing workflows

With these changes has come a new focus on workflows. In OTC markets, where the majority of FX derivatives activity takes place, electronified pricing and risk management have become the norm. In the FX swaps market, for example, participants are used to auto-hedging, algorithmic execution and credit line management through an API on a range of multi- and single-dealer platforms.

Execution in the CLOB of exchanges also offers a highly electronified trading experience, with similar workflows to OTC and anonymized trading against one transparent price point. However, clients might prefer trading away from the orderbook during certain market conditions.

For larger futures positions for example, listed market participants often refer to block trades and EFPs. With FX desks increasingly involved in the brokerage of these trades, there has been a natural push towards low touch workflows that better align with OTC and CLOB execution.

Institutional clients that use OTC FX now expect features like automated uploading and placing to market of orders from their order book management system, as well as receiving allocations in the same format as submitted orders. Much of the OTC FX trade lifecycle is now run by straight-through-processing. As participants in OTC markets make increasing use of EFPs and block trades, the demand for more low touch workflows for trading them is growing as well.

Eurex is encouraging this transition by implementing measures such as simplified exchange rules for EFPs and without a minimum block trade size policy.

These policies are creating greater flexibility to move flow between OTC and listed markets. Firms are able to execute block trades and EFPs bilaterally on electronic multi-dealer platforms, while enjoying STP in the same way that they would in OTC markets or on CLOB.

Ultimately, the market is moving towards platforms where futures and OTC prices can be sourced on one screen, as the harmonization of the FX derivatives landscape takes hold.

This is the third in a series of articles outlining the current view on FX futures. The next article will cover how OTC FX venues like 360T have started bringing FX futures onto their platforms. Subscribe to FX News to receive upcoming articles and updates!

Don't want to miss updates on Eurex FX?

Subscribe to our newsletter on FX highlights, product launches and extensions, as well as news on events and recommended reads.