18 Jan 2024

Eurex

FIC Credit Market Snapshot December 2023

Fed Pivot rally final present for credit investors – Spreads now in overbought territory

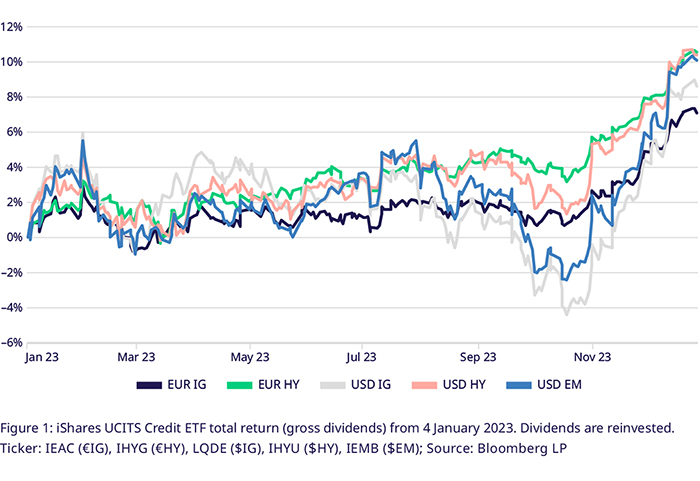

Fed Pivot extends November rally across asset classes over the last month of the year. $-duration gains most. $IG +4.6%, $EM +4.8%, $20yr+ +8.6%

Usually, December is a month with muted activity. This does not necessarily mean that nothing happens in credit and rates markets. Still, portfolio managers and traders trim their exposures before holidays and the new year and tend to avoid jeopardizing gains made over the year. Particularly in the second (tranquil) half of the month, trading volumes typically reduce amid cash-market liquidity drying up. Sometimes, this leads to surprising price swings. However, usually, volatility remains fairly constrained and outsized moves mean-revert quickly. However, this year, there was no time for contemplation and tranquillity as the Fed pivoted from a restrictive to a flexible monetary policy and poised rates for a downward correction. Across developed markets worldwide, Investors were blessed with benchmark yields falling and credit spreads tightening, particularly on higher-yielding names. In the US, the impact of falling yields on bonds with higher duration proved more fruitful than the high carry of shorter-dated high yield bonds. But, the rally extended across high yield and high-grade: $IG (LQDE, +4.64%), $EM (IEMB, +4.83%) and $HY (IHYU, +3.38%) posted significant gains throughout the month. Exposure to the curve itself was rewarded as well, and higher duration bonds gained the most. The $20yr+ US treasury ETF (IDTL, +8.63%) led the $7-10yr (IDTM, +3.69%) and $1-3yr (IDBT, +1.07%) tenors. European markets were subdued in comparison. Both €HY (IHYG, +2.8%) and €IG (IEAC, +2.75%) gained on a yield shift by government bonds and spreads tightening.

Over 2023, high yield bond carry outperformed duration. €HY, $HY, $EM gains more than +10%. $IG +8.6%, €IG +7.1%

Benchmark curves entered 2023 in deep inversion with 2s10s at -60bps in the US, which peaked at -105bps in July. Throughout Q2 and Q3, benchmark treasury yields climbed relentlessly, peaking at 520bps for 2s and 500bps for 10s in mid-October, leading to losses of up to -15% in $20yr+, sending the long-duration $EM and $IG ETFs tumbling. November and December helped cover for the losses and propelled all credit ETF Option underlyings at Eurex into positive territory over the year. Overall, corporate bonds outperformed government bonds, which returned less than 4% in total across $1-3yr, $7-10yr and $20yr+.

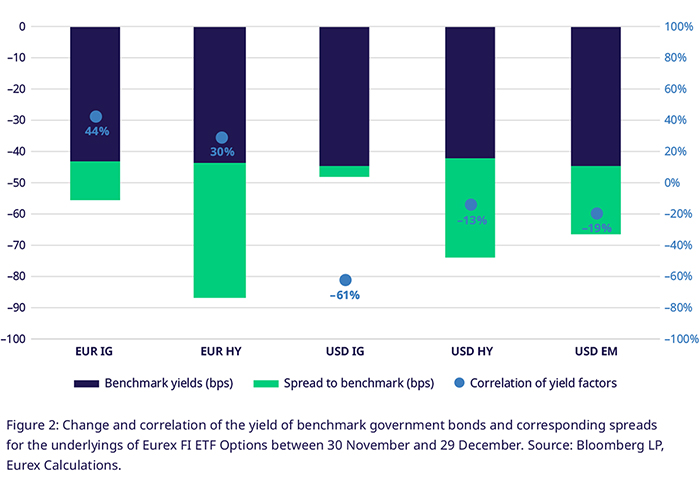

43bps spread compression supported gains from curve movement for €HY, $HY -32bps, $EM -22bps

High grade bonds also appreciated, although $IG was little impacted, with spreads only reducing by 3bps. As in 2022, October proved to be a pivotal month for credit risk, as spreads started compressing mid-month and continued throughout November and December. Over the year, €HY saw spreads decline by 87bps, followed by 67bps for $EM and $HY with 65bps. Credit risk measures for High grade US companies reduced as well, as $IG spreads reduced by ~50bps.

Rate cut expectations baked into December yield drop, leaving yields little room to fall further

Yields rallying may not only have pulled forward profits from carry into higher prices but may well have overshot. Following the December rally, Money market rate traders priced six rate cuts by the Fed and the ECB. These expectations have expressed themselves in the falling benchmark government bond yields in the US and Europe and are already priced in. Since the mid-90s, the only three occasions the Fed cut rates more than five times in a year were in 2020, 2008-2009 and 2001, all periods of severe contractions. Further, economic data has not indicated a significant slowdown. On the contrary e.g., labor market data has shown unemployment receding in the US, so there might be a question of whether aggressive easing is even warranted. This view was shared by FOMC members, as evidenced in the dot-plot of the September meeting, where only one Committee member expected five rate cuts, while the median expectations were three cuts until year-end.

Risk-on-rally that priced out hard-landing leave, credit spreads are now tight >1.6σ and point to reversal

Spreads falling have priced global credit risk on the lower end of the historical spectrum in a short- (1yr) and mid-term (5yr) analysis. The short-term divergence is more pronounced, as basis effects from a spike in spreads last fall have pushed the average in that tenor up. $IG trades especially rich, with spreads more than 2.2σ below the 1yr and 1.3σ below the 5yr average. Similarly, €HY and $EM have spreads 2σ below the 1yr average. Spreads more than 2σ below the 12M average are viewed as overbought and historically indicate that the market has over-rallied and point to a correction in the near future. Over the past ten years, $IG spreads in overbought territory are followed by 40bps in spreads widening over the next six months on average, corresponding roughly to a 2.5% loss. For $EM, the widening is even more pronounced out of overbought territory, with 74bps over the next three months on average, which would correspond to a 4.2% loss from the spread component.

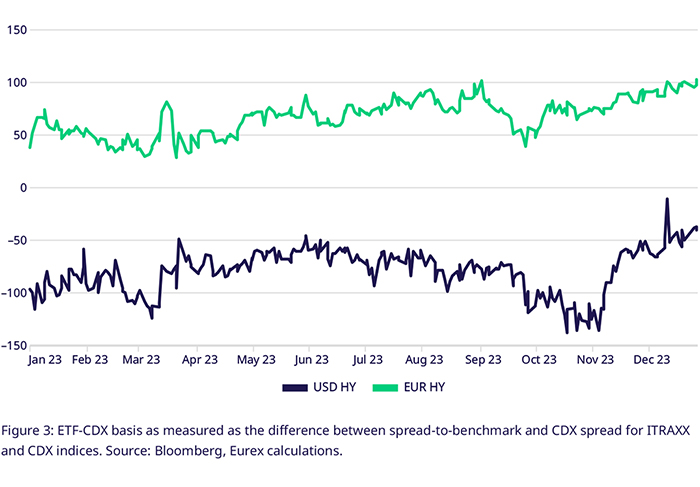

$HY-CDX Basis blips on Fed decision while basis keeps rallying

Both $HY and €HY spreads have rallied less than the CDX counterparts, increasing the basis between the two measures. $-denominated high yield debt has been the only segment where CDX spreads are higher than for the corresponding UCITS ETF underlying. The average spread of CDX HY components fell 46bps to just above 356bps on Dec 29th compared to a rally of just 32bps in $HY. Additionally, the basis blipped around the last FOMC meeting as adjustments permeated across rates and credit markets. Overall, the basis has increased more than 100bps since November's recent low. For €HY, the basis to the ITRAXX XOVER index continued to rally for another 14bps, bringing the 2023 total to around 52bps.

Price for protection against credit-market risk at historic lows. Implied Volatilities end 2023 around 1X realized with Credit-VIX almost 2σ below 1yr average

Implied volatility of put options measures the price for downside protection and is a good gauge of market sentiment. Usually, implied volatility trades at a premium to realized volatility, except in times of highly elevated sentiment or after a short-term crisis has been resolved. 3M at-the-money Options on $HY and €HY are priced at around 70% of the realized annualized volatility over the last 90 days and almost two standard deviations below the 1yr average. CDX Options markets confirm this picture of relative cheapness for credit risk protections. The S&P CVIX indices that track implied volatilities of out-of-the-money Options in CDS indices ended the month almost 2σ below the 12M average. While the $IG and €IG measures stood close to 30 points, $HY and €HY were at around 140.

Utilizing Eurex Credit Futures & Options for Market Positioning

Eurex credit futures and options enable you to hedge existing portfolios against duration and credit risk in one go. Eurex Options on Fixed Income ETFs allow for directional positioning whilst limiting options premium paid with options spreads or more tailored option strategies.

Thinking about trading US Interest rates and volatility using UCITS compliant instruments? Gain exposure to US Treasury markets using the new Options on the IDBT (1-3yr Tenor) and IDTM (7-10yr Tenor) UCITS ETFs.

Contacts